Money should be a good store of value, medium of exchange, and unit of account. There are a lot of barriers preventing bitcoin’s widespread use by the aforementioned criteria, let’s take a look and see how they might be solved.

Lack of Understanding

Bitcoin is complicated and unfamiliar. This is a huge barrier to entry because people distrust what they don’t understand, and ease-of-use and simplicity is what usually sells a new technology. If you have read this series from the beginning though, you may now see some potential upsides to such a drastically different system than what we are used to. Many resisted smartphones for a time (and a few still do). The benefits have to outweigh the costs of adoption, so we may see niche cases being the early adopters (like citizens of Venezuela or remittances payments). Also, when a new complicated technology rolls around, it sometimes takes a generation before it becomes widespread; young people are particularly adept at adopting new tech.

Volatility

The tendency of bitcoin’s price to change rapidly or unpredictably is what comprises volatility.

When you search for bitcoin you may find that most of the results you get (and the discussions happening on forums) are about it’s price. This is understandable, it has seen some crazy moves both up and down over the years facilitating the potential for huge gains (and huge losses). Still, over time the price certainly is increasing. Unless you bought in a single 2 month period in 2013, holding bitcoin for longer than 2 years at any point in its history would land you in a better position than when you started. And, when viewed on a logarithmic scale (used in long-term stock charts), the trend is quite clear:

(Bitcoin Price 2011-2018, Logarithmic Scale)

There is a risk/reward to adopting new tech, and this is no exception. But, my goal is absolutely not to “sell” it to you as an investment by any means.

This is not financial advice. We’re simply looking at the pros and cons of this space, and I encourage everyone to do their own research and come to their own conclusions. Never invest anything you aren’t prepared to lose.

This meteoric rising (and crashing) of the “price” (which, I’ll point out, might just as well be considered an exchange rate) understandably makes it pretty difficult to use bitcoin as a currency. If it moves a few percent in a day, and can move a few hundred percent in a month, purchasing a car or a house could cost you significantly more by the time your finished closing. That’s just not viable, and certainly not a good unit of account.

However, I see the volatility in price simply as growing pains. It is the market that dictates the price of bitcoin, quite literally, it’s traded like a stock. This is referred to as speculation (“the purchase of an asset with the hope that it will become more valuable at a future date”). Speculation happens between national currencies already, but they are generally stable in comparison so it’s not lucrative.

People are unsure of how this whole bitcoin thing is going to play out. It’s not like anything we’ve ever seen, it’s difficult to understand (and use), and it’s not accepted at every corner store or online business. Many in the space are just here for a quick buck, and they sell it when the price rises to get back “real” money we are used to, that is “stable” in price against other currencies, and can predictably buy goods and services.

The way I see it, all of these will concerns diminish in time.

Though Amazon or Target don’t yet accept bitcoin, Microsoft and Overstock.com do. Some cities and towns across the world are embracing it a lot more than others. It’s not surprising to see San Francisco accommodating the new technology. But, other cities like Portsmouth in New Hampshire with numerous cafes and shops accepting bitcoin (and “Dash coin”) might surprise you. There are maps available to see where crypto-currencies are accepted at locations near you, and the amount of them are increasing, albeit slowly. It’s a bit of a chicken-and-egg situation, but that hasn’t stopped revolutions from happening before.

Consider when cars first came about, roads were dirt and mud which cars didn’t do well with. It took building massive infrastructure before cars could ever become mass-adopted, but we spent the time, money, and effort because we saw the potential advantages. It will be trivial for businesses to accept bitcoin compared with pouring hundreds of millions of dollars in asphalt to connect our world. Other parallels include train tracks, phone lines, electricity lines, communication satellites, etc. Each of these replaced or iterated on previous functional technologies, and required massive upfront costs before the benefits were available. It’s clear now that we made some good choices there but there were doubts at the time.

Despite some pretty major setbacks, bitcoin’s trend is up. Interest is growing and more businesses and individuals are actually using it. But due to the trading mentality, the uncertainty with regulations, uncertainty in the technology itself, uncertainty that the price will not drop, and other factors, emotion and greed encourages people to sell in flocks if the price climbs high enough.

Furthermore, right now with a large enough stack of money one can influence this market in drastic ways, and cries of manipulation of the price are not unfounded. So-called “whales” can buy and sell huge amounts of coins and the price can jump a bit each time. Coupled with uncertainty in the space, and so many “investors” trying to time the markets, we end up with a pretty volatile landscape where the price is not stable. My argument is that this is diminishing as it gains in popularity, and it is gaining value because its utility is growing (see “network effect”) and the utility itself is slowly becoming more apparent.

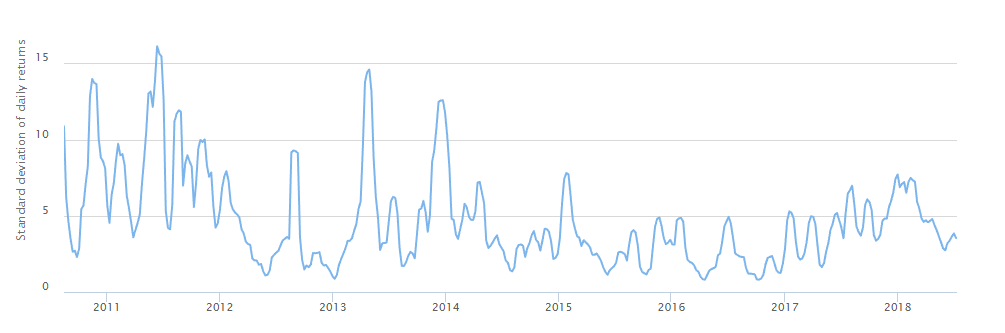

Volatility is actually decreasing.

In the period from 2011 to 2014 bitcoin’s volatility often spikes into the 15% range. But from 2014 to the present, volatility has only just spiked above 7% twice, spending most of it’s time below 5%. Even the large boom and bust in price at the end of 2017 seems tame compared to the early years.

The trends show the price going up over time, and volatility going down. The more actual use the coin has (people saving and buying with bitcoin), the percentage of people entering the space to use it the way it was intended increases, the percentage of “stock traders” declines. And as more capital enters the space, the less influence whales have (because the current against which they swim is getting stronger). And as the price stabilizes, traders will become less interested.

There is a critical point where this becomes a negative feedback loop. I could be wrong, but the idea is at least founded in reality, and it would solve the unit of account issue if the price could stabilize to within a few percent per year.

Similarly, as a store of value, bitcoin becomes more viable in this scenario. This is coupled with the fact that although bitcoin is somewhat inflationary now as the supply is increasing (bitcoins are “discovered” as rewards for mined blocks), the amount of discovered coins are cut in half every few years. This “halving” is logarithmic, meaning eventually the amount of coins discovered is infinitesimally small, and total supply will asymptotically approach 21 million coins (the maximum supply that we will ever see).

This model of supply is actually meant to mimic gold because it’s a well-known store of value and monetary device throughout history (though it is not easily divisible, and not as portable as bitcoin). In both bitcoin and gold, mining is more fruitful in the beginning, and as we extract the low-hanging-fruit, mining requires greater effort and yields less return.

World population is increasing which leads to bitcoin becoming deflationary in the future if demand continues (the supply won’t increase beyond 21 million). And, I argue that it will become more valuable in time due to the network effect as bitcoin use becomes more widespread (the value of being able to exchange with more people anywhere, any time, and without permission from anyone).

This is a positive feedback loop, and shows how bitcoin is deflationary long-term. While deflation is generally considered negative by economists, the main reason is based around debt which isn’t possible in the same way with bitcoin because bitcoins cannot be created out of thin air like fiat currency.

The discussion of deflation vs inflation is an important one, and bitcoin’s monetary policy is an outlier compared with national currencies which are typically inflationary. The US dollar for example averaged 3% inflation since the year 1900. That means that over the last 100 years, a dollar has lost over 95% of its purchasing power. You could buy 95% more stuff with $1,000 last century, or, saving $1,000 from 100 years ago would buy you 95% less stuff at present. Put another way, purchasing power is cut in half after about 25 years, a concern for anyone retiring for over 20 years with a fixed retirement sum.

Some other national currencies have higher inflation rates, and there are numerous cases of inflationary spirals over the years. A few examples include Germany 1923, Hungary 1945, China 1947, Vietnam 1988, Peru 1990, Yugoslavia 1992, Zimbabwe 2008, and right now in Venezuela 2018 (update1: Turkey reaches 100% inflation, update2:Iran inflation approaching 300%).

Entire countries of people have lost essentially all of their money because of uncontrolled government money-printing, and it keeps happening over and over. A wise man would tell you it’s dangerous to say “it could never happen here”.

This is our money with which we hold and exchange value, our earnings, our savings, our livelihoods. Maybe it’s time we had, at least, another option outside of government control. An option that governments can’t destroy through mismanagement. A neutral option that ignores all borders, is open to everyone, and can be accessed anytime from anywhere.

The Fear of “Hacks”

It’s a very real threat to have all your money stolen, if your bank was robbed you are protected by FDIC (in most cases only up to $100,000). The vast majority of coins that have been stolen have come from hackers attacking “exchanges” and getting away with millions. These exchanges are websites where you can trade bitcoin for other crypto-currencies (or “alt-coins”). You can also buy and sell bitcoin on them, and subsequently people end up storing a lot of coins on these exchanges, and the exchanges hold the “private keys” so they can execute trades.

Cryptographic private keys are analogous to a key that opens a door, or, a key that locks a message in a box before it is sent to the recipient. In our case the door opened allows you to sign your message and spend coins, and the message is your transaction on the bitcoin network. Anyone with your private keys can spend your coins. Exchanges are a honey pot of thousands of private keys that represent a lot of money. If a hacker can break into the exchange and steal the keys all at once, their work will pay off.

This is why any crypto guru will advise you not to store large amounts of coins on exchanges, and rather transfer them in your own wallets where you hold the private keys. The mantra is: “your keys, your money; not your keys, NOT YOUR MONEY!”

Of course your own computer can be hacked, but you are not as big a target as an exchange which may hold vast sums of money. There are also some pretty safe ways to store your coins if done right.

Centralized exchanges are a necessary evil for many people because they facilitate acquiring and trading coins easily. But decentralized exchanges are becoming more common because they allow you to trade while keeping your coins in your control at all times. They need some work and more users, but it’s a promising solution to this problem.

Summarizing the above: the big hacks you read about are virtually eliminated if your keys are in your control and you keep them safe.

Fees

Transaction fees are generally negligible in a bitcoin transaction, but in many ways “fees” are holding us back. Interestingly, this is a symptom of being in the very early days.

Firstly, there is a lot of work on “scaling” crypto-currencies (making fees even lower than they already are and increasing transaction speeds). This is just an engineering problem, and many people are working on solving it in many different ways. Other currencies like NANO or IOTA have different underlying tech and have zero fees and instantaneous transactions.

In fact, most fees people encounter aren’t fees from bitcoin transactions; instead, they get hit with fees when exchanging between national currencies and bitcoins. In order to electronically trade USD($), EUR(€), or YEN(¥) with bitcoin, we need to hook into the closed-off for-profit banking network and we need third-parties to do so (and they take their cut).

But even these fees could be avoided in time. For example, you can buy bitcoins with cash directly from a person (localbitoins.com). And, it might seem distant, but in the future you may end up receiving bitcoins as your salary, from a friend, or from accepting them in your place of business. Likewise you can spend your bitcoins directly to other bitcoin users. Getting coins directly eliminates all the exchanging and associated fees because once your money is on the bitcoin network, fees will be negligible (especially as these networks evolve).

Usability

Right now it’s easier than ever to acquire some bitcoin. People can download “Coinbase” or “Square App” on their smartphone and purchase some using a credit card in a few minutes. Depending on which service you use and how much you want to buy, you may need to send a picture of your license for KYC regulations (like you do when you open a bank account). However, as I mentioned above, there are risks to storing all your coins on exchanges, especially with large amounts. I always recommend transferring them to a wallet where you control the private keys.

But using wallets and storing private keys (and “seeds”) securely, is not as straightforward as we would like. This is a major factor holding back adoption, because if it’s not easy to use, people will consider it too much effort.

The next post in this series digs into wallets and storing your coins.